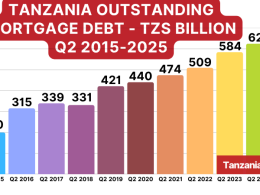

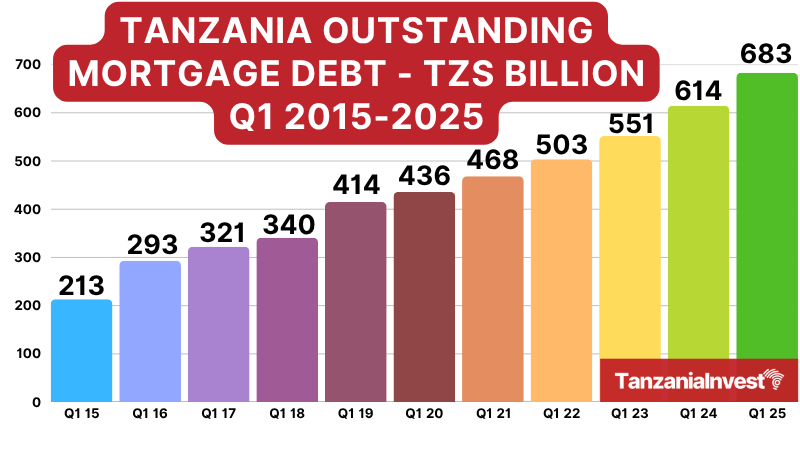

In the first quarter of 2025, the mortgage market in Tanzania registered a 3.6% growth in the value of mortgages provided by the banking sector for the purposes of residential housing compared to the last quarter of 2024.

The value in residential mortgages went from TZS 659.30 billion recorded on 31 December 2024 to TZS 683.03 billion (US$ 266.24 million) on 31 March 2025.

This was indicated in the Tanzania Mortgage Market Update – 31 March 2025, recently released by the Bank of Tanzania (BOT).

On a year-to-year comparison, a growth of 11.4% was registered in the value of mortgage loans between 31 March 2024 and 31 March 2025.

Tanzania Mortgage Market Demand and Supply in Q1 2025

The Update explains that the demand for housing and housing loans remains extremely high as it is constrained by an inadequate supply of equitable houses and high-interest rates charged on housing loans.

Most lenders offer loans for home purchase and equity release, while a few offer loans for self-construction, which continue to be expensive and beyond the reach of the average Tanzanian.

While interests on residential mortgages improved from 22–24% in 2010 to 13–19% offered today, market interest rates are still relatively high hence negatively affecting affordability.

Additionally, cumbersome processes around the issuance of titles (especially unit titles) continue to pose a challenge by affecting borrowers’ eligibility to access residential mortgages.

Further, competition in the market has led to the emergence of other products that are impacting mortgage market growth as the products have favorable terms than mortgage products and are used for housing purposes.

These products compete with mortgages in terms of loan amount and, to some extent, tenor as they are offering consumer loans for up to seven years, amounting to more than TZS 150 million, an amount enough to buy a housing unit.

The competition comes from the ease with which competing products, specifically, consumer loans, are available relatively easily compared to the lengthy process experienced in mortgage loans, as well as additional costs in mortgage loans, including registration costs, valuation fees, and insurance costs, which are not applicable in consumer loans.